AMLA Data Collection and Testing Exercise

Testing the Future EU AML Supervisory Framework

In March 2026, the European Anti-Money Laundering Authority (AMLA) launched a data collection and testing exercise designed to calibrate its EU-wide money laundering and terrorist financing (ML/TF) risk assessment models.

The exercise represents one of the first operational steps toward the new European AML supervisory architecture created by the EU AML Package. Its primary objective is to develop a harmonised methodology for assessing ML/TF risks across credit and financial institutions in the European Union.

The data collected will help AMLA build the models used to select institutions for direct EU-level supervision starting in 2028.

Why AMLA Is Collecting Data

AMLA’s testing exercise serves two key regulatory purposes.

1. Calibration of AMLA Risk Assessment Models

The first objective is to test and calibrate AMLA’s ML/TF risk assessment models. These models are intended to ensure that supervisors across the EU apply consistent risk indicators and comparable methodologies when assessing financial institutions.

Historically, risk assessments were conducted primarily at national level, often using different supervisory frameworks and indicators. AMLA aims to introduce a common EU-wide analytical approach based on structured datasets.

2. Preparation for AMLA Direct Supervision

The second objective is to support the selection process for institutions that will fall under AMLA’s direct supervision.

Under the new EU AML framework, AMLA will directly supervise a limited number of high-risk cross-border financial institutions. The selection process will take place in 2027, with direct supervision beginning in 2028.

The testing exercise allows AMLA to validate the data requirements and methodologies before this selection process begins.

Who Participates in the AMLA Exercise

Participation in the data collection exercise is limited to institutions that have been notified by their national competent authorities.

The participating entities are part of a representative sample of credit and financial institutions across the EU. The sample includes both:

- institutions selected by supervisors based on supervisory relevance, and

- randomly selected entities to ensure statistical representativeness.

If an institution has not been notified by its national authority, it is not part of the exercise.

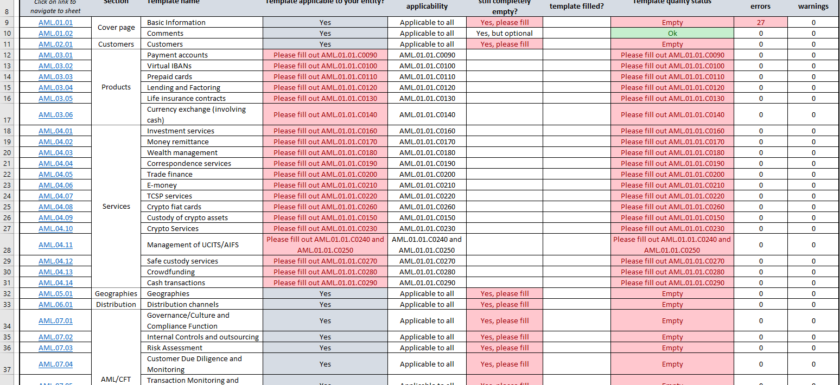

The AMLA Reporting Package

To support the testing exercise, AMLA has published a reporting package that includes several components.

Interpretative Note

The interpretative note explains the risk assessment methodology and reporting instructions. It provides definitions, clarifies the scope of the data collection, and explains how institutions should interpret the requested datapoints.

Reporting Template

The reporting template contains the structured data fields that institutions must complete. These templates capture information across multiple AML risk dimensions.

Webinar and Presentation Materials

AMLA has also provided a recorded webinar and presentation slides to guide participating institutions through the reporting requirements and explain the overall methodology.

What Data AMLA Is Collecting

The data collection exercise captures information across multiple risk dimensions relevant to ML/TF exposure.

Institutional Characteristics

Institutions must report structural information about their organisation, including:

- type of financial institution

- services and products offered

- geographic footprint

- cross-border activities.

These datapoints help AMLA assess institutional risk profiles.

Customer Risk Indicators

The reporting templates also include information about the customer base of institutions, such as:

- number and type of customers

- exposure to politically exposed persons (PEPs)

- customers linked to high-risk jurisdictions

- complex ownership structures.

These indicators help assess customer-driven ML/TF risk exposure.

Product and Service Risk

AMLA also collects data on financial products and services offered by institutions, including payment services, lending products, insurance contracts and other financial activities.

These datapoints allow AMLA to analyse product-related ML/TF risks.

AML Control Environment

In addition to inherent risk indicators, the reporting framework includes information about AML governance and control systems, such as:

- customer due diligence processes

- transaction monitoring systems

- sanctions screening

- internal AML controls.

This information helps AMLA assess risk mitigation and control effectiveness.

Timeline of the Exercise

The AMLA testing exercise follows a defined reporting schedule.

Participating institutions are required to submit their data by 22 April 2026.

After submission, AMLA will:

- review the completeness and quality of the data,

- test the proposed risk indicators and models,

- refine the methodology based on the results.

The insights gained from this exercise will support the final development of AMLA’s supervisory risk models.

Why the AMLA Data Collection Matters

The AMLA testing exercise marks an important step toward data-driven AML supervision in the European Union.

For the first time, the EU is building a centralised supervisory risk assessment methodology based on structured reporting from financial institutions.

The exercise allows both AMLA and participating institutions to:

- test internal data systems and reporting capabilities,

- identify gaps in AML risk data,

- ensure that institutions can produce the information required for future EU-level supervision.

Ultimately, the initiative lays the foundation for a harmonised and analytical approach to AML supervision across the EU financial sector.

Downloads

Source: https://www.amla.europa.eu/amla-launches-data-collection-exercise-test-risk-assessment-models_en